Cutting Through The Noise Of Financial Markets

Stocks in focus

ADMA Biologics Overview

ADMA Biologics is a U.S. biopharmaceutical company specialising in the development, manufacturing, and commercialisation of plasma‑derived biologics used to treat immune deficiencies and infectious diseases. Human plasma the yellowish fluid that makes up about 55% of blood volume carries red and white cells essential for immunity. Transforming plasma into usable therapies is a complex, multi‑step process. To maintain control and quality across every stage, ADMA employs a vertically integrated model, overseeing plasma collection, manufacturing, and distribution through its ADMA BioCenters and production facilities.

FDA‑Approved Products

- BIVIGAM® – Intravenous immune globulin (IVIG) for primary humoral immunodeficiency (PI).

- ASCENIV™ – IVIG for PI, differentiated by a proprietary plasma selection process.

- Nabi‑HB® – Human antibody therapy for post‑exposure prophylaxis against Hepatitis B.

ADMA’s strength lies in its FDA‑approved portfolio, proprietary plasma technology, and vertically integrated supply chain.

Price Action

Prior to 2024, ADMA was burning cash through R&D and manufacturing scale‑up investments. In 2024, the company successfully transitioned from concept to commercial profitability, becoming a high‑growth plasma therapy leader. This breakout reflected structural improvements in revenue, margins, and supply chain stability, and investors quickly seized the opportunity to back a company entering commercial‑scale profitability earlier than expected.

In 2025, performance has slowed compared to the explosive 400% run of 2024. Investor caution and profit‑taking were natural after such a surge, with concerns that valuations may have stretched too far. However, demand for plasma‑derived therapies remains strong, and the FDA’s approval of ADMA’s yield‑enhancement process has renewed optimism about future production efficiencies.

Fundamental Analysis

The slower pace in 2025 has allowed ADMA’s fundamentals to catch up with its prior share price surge. While some investors remain skeptical about valuation, sentiment has normalised, bringing the stock back to healthier levels.

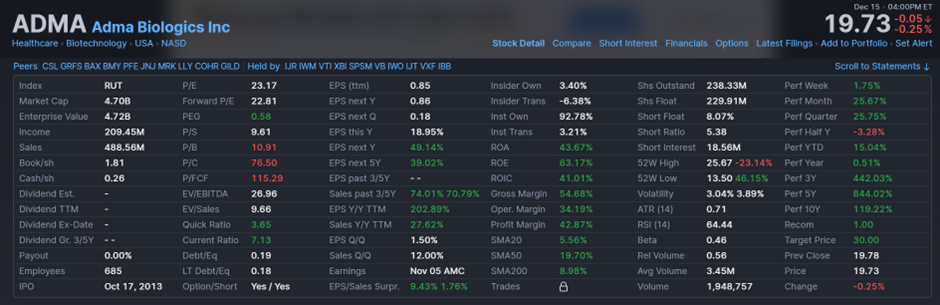

Key metrics:

- Return on Equity (ROE): 63.17%

- Profit Margin: 42.97%

- Projected EPS Growth (5 years): 39.03%

- P/E Ratio: In line with healthcare industry averages

- P/FCF: 115.29, reflecting growth‑mode reinvestment rather than near‑term dividend potential

Overall, ADMA’s fundamentals now better align with its valuation, supporting a positive outlook.

Highlighting the margins

As noted earlier, ADMA operated at a loss for several years. For early investors, however, this phase was seen as a necessary commitment a compulsory investment in building the foundation for the margins the company now delivers.

- Gross Margin: 54.68%

- Operating Margin: 34.19%

- Profit Margin: 42.87%

These are robust figures, and there are clear reasons behind them. Applying Porter’s Five Forces highlights two key dynamics:

- Low bargaining power of buyers – ADMA’s FDA‑approved portfolio faces limited direct competition, meaning customers have few alternatives.

- Reduced bargaining power of suppliers – By heavily investing in a vertically integrated supply chain, ADMA controls nearly every stage of production. Aside from sourcing raw plasma, the process is managed in‑house, giving the company far greater control and efficiency.

In short, ADMA’s strong margins are the result of deliberate strategy, not chance. With its differentiated products and integrated operations, these margins are well positioned to remain resilient over the coming years.

Strategic Outlook

ADMA’s strategy emphasizes manufacturing scale‑up, plasma collection expansion, and long‑term revenue growth rather than headline acquisitions. Management continues to invest in its BioCenters network and secure long‑term plasma supply contracts to ensure raw material availability. While no major new projects were announced in 2025, scaling plasma collection capacity remains a critical growth lever.

Summary

ADMA’s FDA‑approved product portfolio, proprietary plasma technology, and vertically integrated supply chain position it well for the future. Although growth will be more measured compared to 2024, the company’s valuation still modest at under $5 billion leaves room for expansion if earnings continue to rise. The slower year in 2025 has allowed fundamentals to catch up, reinforcing confidence in ADMA’s long‑term trajectory and positive outlook.

Risks to Consider

- Regulatory Oversight: Plasma‑derived biologics are subject to strict FDA and international regulation.

- Competitive Pressure: ADMA faces competition from global plasma leaders such as CSL, Grifols, Octapharma, and Takeda.

- Market Volatility: Insider share sales in 2025 have heightened investor caution, contributing to price swings.

Disclaimer: The content provided on Whisper Wealth is for informational and educational purposes only and does not constitute financial, investment, or legal advice. While I strive to provide accurate and timely information, I am not a licensed financial advisor, and the views expressed are my own. You should not rely solely on this content to make financial decisions. Always consult with a qualified financial professional before making investment choices. Whisper Wealth and its contributors are not responsible for any losses or damages resulting from reliance on this information.